AFR's Banking Crisis of '23 Brief: 18th Edition

A cogent email of curated information on the banking crisis and the response

First Republic Sale Highlights Finreg Problems

The purchase of First Republic by JPMorgan Chase may have solved a problem — time will tell — but there was collateral damage that we would not have to contend with, had the right laws and regulations been in place. There was a $13bn hit to the deposit insurance fund. And this latest act brings to light structural problems that continue to plague the system. The short of it: the big (banks) get bigger.

AFR noted that the First Republic sale underscores the need to get a handle on megabank risk and financial sector concentration. Boosting capital, new bank merger guidelines and action on too-big-to-manage could help create a system in which this bad choice would not have been necessary. So would breaking up the biggest banks.

“Federal authorities have a number of tools designed to manage the risks of Wall Street’s megabanks to the financial system,” said Alexa Philo, senior policy analyst at Americans for Financial Reform Education Fund and a former Federal Reserve Bank of New York examiner. “They need to use those tools promptly, and err on the side of caution, especially since the financial system has already shown significant instability already this year.”

Jamie Dimon hopes “this mini-bank crisis is over”. Maybe. Today, a number of mid-size bank stocks tanked. As of now, there are “no obvious candidates” for further trouble per Politico, and NYT’s autopsy finds its rivals on “firmer footing.” Also: hedge funds are still shorting bank stocks, per NYT Dealbook.

Is the Fed’s apparent plan to keep tightening going to stress more institutions, wonders NYT’s Peter Coy? Could be. Groundwork Collaborative points out that at the very least, the plan risks harming labor unnecessarily.

Karen Petrou of Federal Financial Analytics highlights how regulators at the Fed and FDIC had few options with a bank of First Republic’s size without making the big bigger. She tweets: “FDIC knows it can’t do this w/o consolidating market power in the very largest banks but has do nothing but talk about it.”

Warren tweeted: “The failure of First Republic Bank shows how deregulation has made the too big to fail problem even worse. A poorly supervised bank was snapped up by an even bigger bank—ultimately taxpayers will be on the hook. Congress needs to make major reforms to fix a broken banking system.” And Waters calls on the failed banks’ CEOs to testify.

The FDIC cut JPMorgan a very good deal on First Republic and the government had to foot a sizable part of the bill. Bloomberg dissects the deal here with a lot of numbers.

Richard Bookstaber raises the high-level issue of the regulatory system’s shortcomings on risk management. But, remember: this crisis is a political problem, not merely a technical one. Lobbying and regulatory friendliness toward the banks brought us here.

Morgan Ricks wonders if regulators really figured out the least-cost solution and explains how JPMorgan/big banks benefited.

Barr and Executive Compensation – Shadow Banks – Deposit Insurance – Further Investigation – Fed Shuffling – Crypto – FOMC Conflict of Interest Rules – AI vs. Finance – Confidence in the Fed – Social Media Bank Runs – Timelines and Size of Bank Failures

Feedback? Reach us at afrbrief@ourfinancialsecurity.org

Barr and Executive Compensation.

Easily lost in the shuffle: The Fed’s postmortem on SVB tackles the topic of executive compensation and confirms that current incentive compensation structures can encourage reckless risk-taking in the financial system:

“The incentive compensation arrangements and practices at SVBFG encouraged excessive risk taking to maximize short-term financial metrics. SVBFG’s compensation practices also did not adequately reflect longer-term performance, nonfinancial risks, or unaddressed audit or supervisory issues.”

Dodd-Frank Section 956 has laid dormant for 12 years without a final rule from regulators. It’s time to act, per a letter from AFR and 24 other groups. Additionally, with particular heed toward the SVB collapse: a ban on stock options, prohibiting hedging bonus pay, and clawbacks. Noting that some bonuses, were paid out the same day that the bank failed, Barr writes:

“Stronger or more specific supervisory guidance or rules on incentive compensation for firms of SVBFG’s size, complexity, and risk profile–or more rigorous enforcement of existing guidance and rules–may have mitigated these risks.”

Efforts to clawback compensation from execs at failed banks like SVB have some momentum in the Senate. Warren introduced a bipartisan bill in late March, the Failed Bank Executives Clawback Act. Sens. Reed and Grassley also rolled out their own clawback bill. Rep. Velázquez and Sen. Hollen have also called for Section 956 implementation, in a letter to regulators.

Shadow Banks.

International regulators have been pretty outspoken of late on keeping our guard up regarding trouble in the shadow banking sector. Tip of the iceberg?

Nice explainer here from WSJ. Key point: “Banks are the most visible debtholders, but, collectively, just as much debt is held by pension and mutual funds, private-credit funds, life insurers, business-development companies, hedge funds, and other nonbanks—or, as they are sometimes called, shadow banks.”

Private credit is not insulated from the risk of heightened interest rates. See here for an AFR report covering this explosive phenomenon. A helpful Twitter thread highlights the issue of leverage in private credit.

IMF Managing Director Georgieva warned of other potential vulnerabilities opening up among nonbanks. FSB chair Knot believes the global financial system could use a “massive adjustment” to withstand the pressure of higher rates and is likewise wary of opaque nonbanks.

Deposit Insurance.

The FDIC released its overview of the deposit insurance system in the wake of the bank failures. The report outlines three possible avenues of reform: continuing limited coverage with the possibility of an increased cap, unlimited coverage, or targeted coverage tailored to account types. The agency finds that targeted coverage may be the most effective. Gruenberg issued a statement in time with the release of the report, citing “regulation, supervision, and deposit insurance pricing” as “essential” to allowing the system to meet its financial stability goals.

Further Investigation.

Reps. Comer and McClain of House Oversight and Accountability have opened an investigation probing the role of the San Francisco Fed, where CEO Greg Becker served as a director, in SVB’s collapse. The two lawmakers sent a letter to the SF Fed’s president and CEO Daly requesting documents and information pertaining to its oversight of the collapsed bank. The letter raised alarm at the inaction despite MRAs and MRIAs piling up at their doorstep.

“Regulators filing MRAs and MRIAs may have been responding to knowledge that, at the end of 2022, almost 96 percent of deposits held at SVB were uninsured, making the bank susceptible to a run. While the signs of significant and alarming risk were clear, no regulator used more severe tools, such as fines or consent orders, to require action from SVB.”

Related: Forbes contributor Mayra Rodriguez Valladares highlights the need for SVB CEO Becker to appear before Congress. Lots of burning questions.

Fed Shuffling.

The Biden administration may be making headway on appointments to the Fed. A promotion to vice chair for Federal Reserve Governor Philip Jefferson is under consideration. That would leave a spot on the board open for, according to sources familiar with the matter, a possible Latino economist, which would satisfy Sen. Menendez’s calls. Nothing is set in stone, however, and earlier contenders — such as Northwestern Prof. Janice Eberly — are likely still on the list.

Crypto.

While Coinbase and the SEC duke it out in court, House Financial’s McHenry wants to get the stablecoin bill out of committee by the end of June.

FOMC Conflict of Interest Rules.

The Fed thinks that FOMC’s investment and trading rules could use a redesign to root out conflicts of interest, according to an evaluation report from OIG. The report provides recommendations to shore up Fed banks’ ability to monitor personal investment and trading activity.

AI vs. Finance.

Economists at the Richmond Fed believe that ChatGPT has an aptitude for interpreting “Fedspeak” – when a central banker makes a comment that mere humans must scramble to decipher – according to a new research paper. While it can spit back the correct answer on a “standardized test of economics knowledge” 87 percent of the time, researchers warn that it’s prone to mistakes and shortcomings. FT explores the danger of relying on AI to tell us about finance. Some major dangers, they write: the non-transparency of AI tools, the threat of concentration risk in the AI market, and the fear that regulators couldn’t keep up. And in comes JPMorgan with a Fedspeak-parsing AI of its own, looking back at decades of speeches, for the purpose of trading and speculation.

Confidence in the Fed.

Actually, fairly little of it from economist Joseph Stiglitz. He writes that regulators “have failed to keep the banking system safe” and presses for “meaningful reforms of deposit insurance, regulation, and governance.” Stiglitz also argues that federal assessments — banking supervision — are a public good:

“Most people do not have the ability, resources, or access to information needed to assess the soundness of banks. Such assessments are a fundamental public good and, as such, the government’s responsibility. If a bank can accept the public’s money, the public should have confidence that it can repay it.”

Social Media Bank Runs.

WSJ touches on the academic paper published last week, echoing the notion that light-speed communication amplified the “fear of the unknown” that triggers bank runs. There’s an interview with one of the co-authors too. The line of thought is friendly to the bank lobby’s smokescreen which, of course, is a no-good distraction from the real, regulatory and policy issues. No shortage of previous discussion here and here.

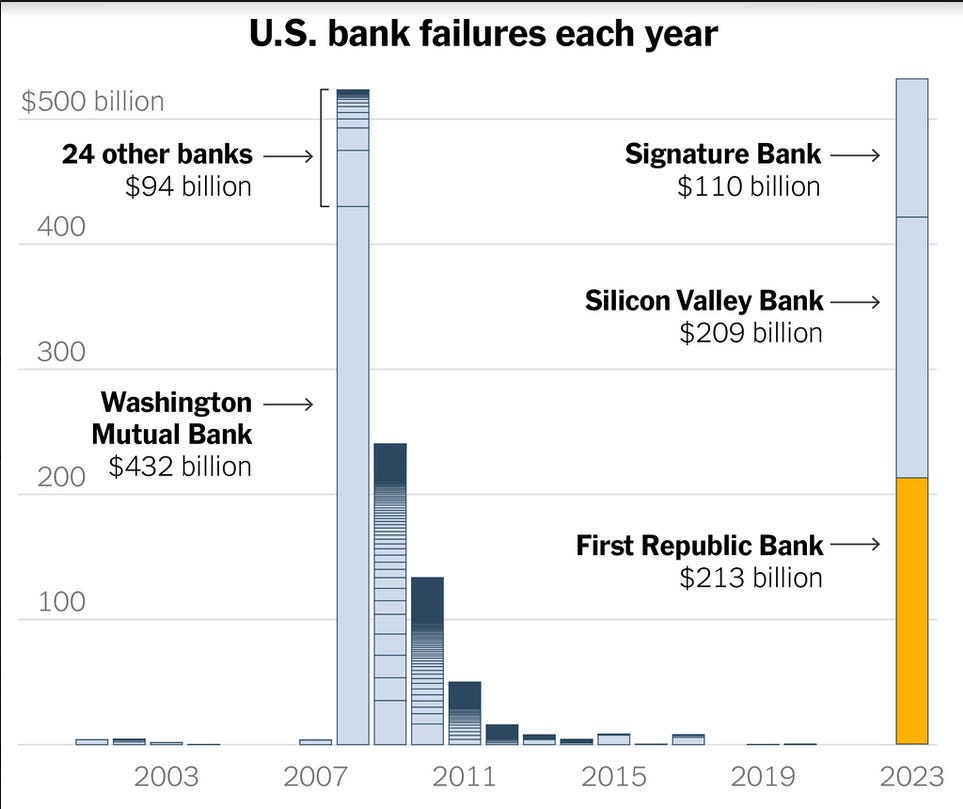

Timelines and Size of Bank Failures.

NYT has a useful retrospective timeline for anyone looking to freshen up on what’s happened so far since March. And, also, an interesting graphic by Karl Russell on the number of bank failures a year in their newsletter, gleaned from FDIC data. See here: