Financial Justice, 24th Edition: Smaller Banks, Better Regulation, More Fairness

The Washington Monthly has published an article by a staff member at Americans for Financial Reform that drives at the other side of the deposit insurance coin, pardon the money pun. Chock full of links on key issues and some very relevant history:

Blaming deposit insurance itself, however much the rescue of SVB depositors sticks in the craw, would be precisely the wrong reaction to this year’s crisis. The true injustice of the moment lies not in extending deposit insurance but in the paucity of obligations that bankers face in return. If we’re going to put the full faith and credit of the United States behind the banks, then our democratically elected government needs to bring the ethos of deposit insurance to bear and give the rest of us the financial system we deserve. Making banking the business of all Americans is not merely smart policy that would give us a more stable, fair, and equitable system. It embodies American values with a long and noble pedigree—ones we would do well to live out in our own time.

We could start to realize needed changes to the financial system by breaking up the biggest banks. Alas, the recent news – looking at you, Treasury Secretary Yellen – is not good. See the first item here for details.

Editor’s note: Today we are changing the name of this newsletter to Financial Justice. The name is an homage to Financial Justice: The People’s Campaign to Stop Lender Abuse, a book about the foundation of Americans for Financial Reform in early 2009, and the passage of the landmark Dodd-Frank law.

FINANCIAL STABILITY: Banker Mergers – MonPol and Finreg – JPMorgan – Banking Crisis Lessons – Deposits – Deposit Insurance – Regionals – Commercial Real Estate – Credit Default Swaps – Project Colony – A Banker’s Lifetime Ban

CONSUMER: Cashing Checks – CFPB and AI – “High Risk Hustling”

PRIVATE EQUITY: PE Lenders – The Fourth Exit

CRYPTO: First Broker-Dealer – Sam Bankman-Fried

HOUSING: Housing Bust – Fannie and Freddie Fees – Renters’ Paradise

POLITICS AND MONEY: Tim Scott – Glenn Youngkin

Feedback? Reach us at afrnews@ourfinancialsecurity.org

FINANCIAL STABILITY

Bank Mergers.

Yellen told bank executives that more bank mergers may be necessary. Biden policy is to reinvigorate antitrust laws, so Yellen is – apart from pushing bad policy – out of step with other members of the administration.

It’s not hard to imagine Yellen getting the Michael Hsu treatment from Sen. Warren over these comments. Why did Yellen articulate this stance at this moment? It does come as Wall Street types and their allies have stepped up the public case for mergers … The chattering classes are also insisting the United States is “overbanked.” Why on earth would we let banks get bigger as we grapple with changes aimed at improving financial stability? The choice isn’t between mergers and pursuing some radical thing. Just say no.

Assistant AG Jonathan Kanter is giving a speech on June 20 about banking consolidation. The invitation suggests a tougher approach than Yellen. The teaser: “Many of the largest financial institutions are growing even bigger. This year’s high profile bank failures have heightened concerns about banks that are ‘Too Big to Fail,’ while drawing larger questions about what the future of the banking industry will or should look like.”

American Economic Liberties Project policy analyst Shaheed Naeem rails against further consolidation. Good.

MonPol and FinReg.

There’s now a financial stability test for monetary policy, one that came into play a lot faster than the question of employment. Bloomberg: “Federal Reserve policymakers are increasingly grappling with a critical question: How much should they weigh the adverse impact of their interest-rate hikes on banks against the goal of containing the fastest price increases in decades?”

Powell remains open to a potential pause on rate increases, per WSJ. Inflation remains far from the 2% target. CME Group’s FedWatch tool predicts a high likelihood of rates holding at current levels.

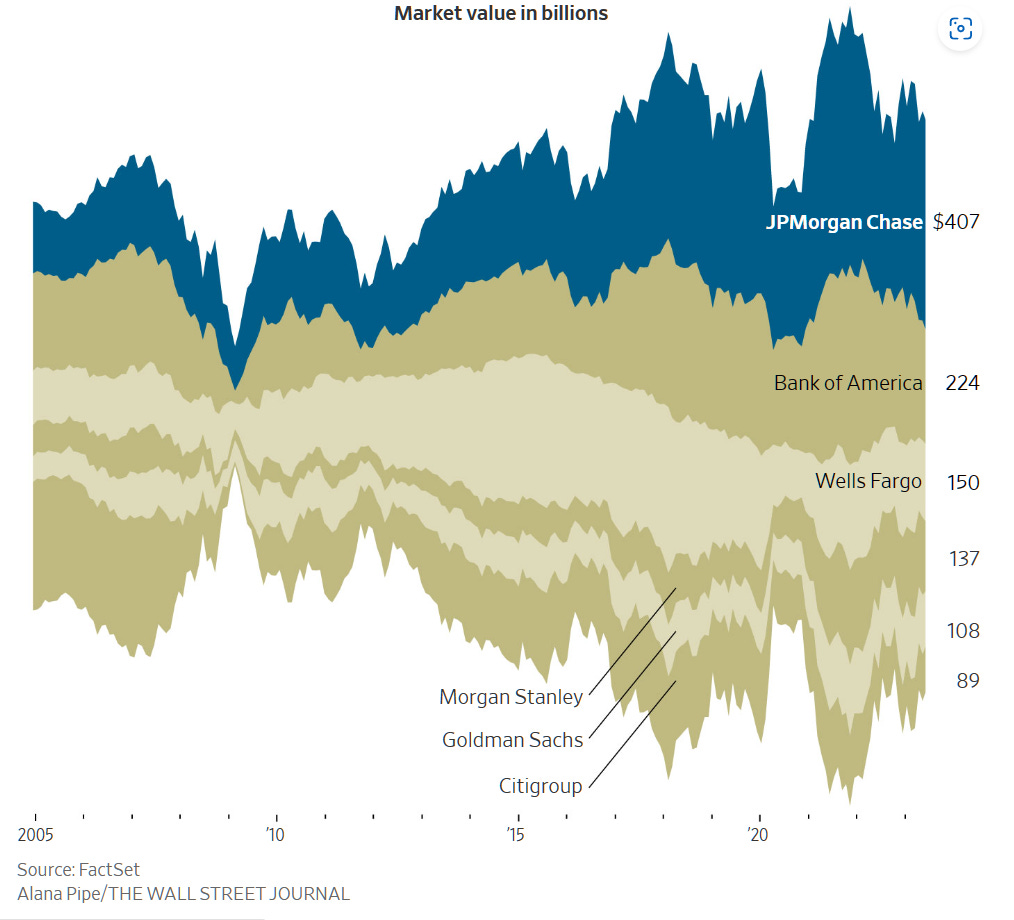

JPMorgan.

WSJ details how the banking crisis has served to empower … JPMorgan! Sitting close to 4,800 branches, it holds more than 13% of the nation’s deposits and 21% of credit card spending after its First Republic buy. While outflows shocked midsize regionals, JPMorgan saw inflows of $50bn in new deposits. Reminder: Mega-brain Adam Tooze calls it “not just the largest non-Chinese bank by size. It is also a universal player with a powerful position in investment banking, retail banking, and asset management.”

Warren wrote a detailed letter to FDIC’s Gruenberg and OCC’s Hsu probing the rationale behind the First Republic sale to JPMorgan. Since the sale, the megabank expects to make $84bn in net interest income this year alone.

With a market value greater than Bank of America and Wells Fargo combined, JPMorgan is only expected to continue its expansion, according to WSJ. First Republic’s wealth management arm was of particular interest to JPM’s analysts in its efforts to reach the rich not already captured by its consumer banking programs. Asset management is an area where JPMorgan sees potential for growth.

Banking Crisis Lessons.

Minneapolis Fed president Kashkari details his worries about too-big-to-fail and offers an alternative to what he views as “doubling down on a complex system of rules for banks that provide the illusion of stability”: increasing equity capital. Kashkari writes that while it is difficult to predict and prepare for all types of shock, shoring up capital can protect against virtually all scenarios.

Higher capital levels can both address the too-big-to-fail advantage of the largest banks (which stunningly tend to have much lower levels of capital than small banks have) and can reduce the complexity of our regulatory apparatus. Complexity is not an indicator of resilience; it is an indicator of fragility, masquerading as sophistication. Banks hate higher levels of capital because the amount of capital inversely affects their stock prices, and they will thus fight higher capital requirements with all their mighty influence.

Stanford’s Anat Admati joins London Business School prof. Richard Portes and Max Planck Institute director Martin Hellwig in a letter to FT suggesting that it isn’t bank runs that threatens stability, but banks’ underlying insolvency. This year’s bank failures, they write, “illustrate the fragility of using deposits and other short-term debt with razor-thin equity funding to make long-term investments.” They cite studies indicating that the banking system would show $2tn in losses if institutions suddenly had to mark their assets to market.

Admati, Portes and Hellwig dive deeper into the insolvency and liquidity risks brought to bear by SVB for a Center for Economic and Policy Research piece:

Today, policymakers, lobbyists, and commentators seem to miss the obvious lesson: ignoring insolvencies while also insuring deposits can lead to disastrous outcomes. The Federal Reserve is now providing liquidity support without restoring solvency… Expanding deposit insurance without eliminating zombies is similarly problematic. If bailouts of uninsured depositors continue, the extra levies on the banking industry to cover losses to the insurance fund may harm the viability of remaining banks.

WSJ notes the banking crisis brought to light a false assumption long-held by bank execs and regulators: That higher interest rates means higher values for deposit businesses. Many believed hiked-up rates would grow franchise values in “a natural hedge against the declining market values of a portfolio of fixed-rate loans and bonds.”

Deposits.

The Fed released its H.8 overview of commercial banks’ assets and liabilities last week. WSJ’s Nick Timiraos offers up charts which show that deposits at banks smaller than the top 25 have been stable since April, as of May 10, unless you exclude jumbo CDs (>$100,000). Doing that shows declines in lower-cost deposits.

Deposit Insurance.

An op-ed from UC Berkeley professor Prasad Krishnamurthy signals that all deposits in the U.S. are insured, even if the legal limit says otherwise. He cites Yellen’s March 16 announcement that uninsured deposits would be protected if the alternative was the proliferation of systemic risk. His solution: progressive insurance for large deposits, in which the FDIC would assess a “risk-based fee to banks on the basis of their large deposits and any other factors that predict insolvency.”

Regionals.

Columbia prof. Kate Judge calls the regional banking model unsustainable and that community banks are demonstrating stability.

“We saw depositors were leaving regional banks… But the small community banks were really holding onto those deposits and they managed to continue to provide meaningful credit.”

Commercial Real Estate.

NYU prof. Arpit Gupta examines the potential threats caused by the ailing $20tn commercial real estate market, to which banks are very exposed. The decline spurred by heightened interest rates, vacancies and “the costs of regulation” inherent in a green transition. Gupta has a recommendation: subsidizing properties that “have a bright future once repositioned,” essentially using taxpayer dollars to turn the empty space into more useful buildings.

Workers are returning to the office but at a slow pace, enough so that vacancies remain high and investors bet on commercial real estate stocks falling. Coupled with a dip in rents, Q1 leasing activity for office real estate investment trusts fell 20% quarter-on-quarter. Growth appears limited; firms that primarily own offices have begun diversifying their portfolios.

Even the most creditworthy property investors may default, according to WSJ. Some larger investors are cutting loose their buy-in to shield against losses.

Credit Default Swaps.

The International Financing Review suggests the Credit Suisse turmoil exposes the shaky infrastructure on which the $10tn credit derivatives market stands now that the Swiss bank is out of the picture. After its collapse, the Credit Derivatives Determinations Committee has been asked twice whether default swap payments on the bank’s debt had been triggered. Both attempts failed, with fewer members on the Committee to vote with the decline of the CDS market.

Project Colony.

This Easter, dozens of bankers at SVB’s new owner First Citizens tendered their resignation and were promptly taken in by the British multinational HSBC Bank in a scheme reportedly called “Project Colony.” Now, First Citizens is suing HSBC for more than $1bn for a “scheme to plunder.”

A Banker’s Lifetime Ban.

After a lower court upheld a lifetime ban from the industry against a Michigan banker for lending practices that cost his bank more than $6mn, the Supreme Court stayed the penalty after finding that the FDIC made “two legal errors in adjudicating” his case. The case goes back to the FDIC Board for further review.

CONSUMER

Cashing Checks.

A paper in MIT Press finds that just one extra day in the time it takes for a check to clear pushes nearly two-thirds of account holders more likely to turn to cashing a check instead of depositing it. Aaron Klein sums it up, making the case for faster payments: “Making all checks clear within 1 day would reduce demand for check cashers by 55% among the 70% of check cashing customers with bank accounts.”

CFPB and AI.

An American Banker article calls on the Consumer Financial Protection Bureau to start using AI to reduce lending discrimination. Worth noting: the writer is a VP at a company that touts “AI-driven lending” for “more accurate risk prediction, faster credit decisions, and more inclusive lending.” Ingrained bias has long been an issue in financial sector artificial intelligence.

“High Risk Hustling”.

The name of a new paper in CUNY Law Review that explores how U.S. banks financially discriminate against sex workers, targeted by algorithms, maliciously flagged, or any number of other prejudicial tactics.

Internationally, peer-led sex worker organizations have documented payment processors that discriminate, collating public policies and user experiences. They report refusals of merchant services, being unable to open accounts, being denied loans, finance or insurance, higher premiums, and having money frozen, withheld or forfeited.

PRIVATE EQUITY

PE Lenders.

A pullback on lending by big banks during the crisis has allowed non-bank lenders, including private equity, to fill their vacancies. Private credit already represents 12% of the U.S. commercial credit market, with new growth on the horizon.

The Fourth Exit.

Besides mergers/acquisitions, initial public offerings or sales to other investors, private equity uses a fourth exit strategy by way of continuation funds, or secondary funds. Demand for fourth exits skyrocketed during the early pandemic, from $20bn in 2020 to $60bn in 2021. Now, a new SEC proposal would make the tool less appealing to these firms. The rule would require fairness opinions before the creation of these vehicles.

CRYPTO

First Broker-Dealer.

Politico reports the Financial Industry Regulatory Authority designated Prometheum Ember Capital as a special-purpose broker dealer for cryptocurrency, making it the first FINRA member and SEC-registered broker-dealer able to safeguard crypto securities. Prometheum CEO Kaplan says that it offers evidence that there may be clarity about SEC rule compliance.

Sam Bankman-Fried.

Prosecutors have amassed a dossier of over six million pages of records in the case against the collapsed crypto exchange’s founder ahead of an October trial. It’s one of the largest ever hoards of evidence in a securities fraud case; prosecutors against Martha Stewart in 2004 only came up with 525,000 pages of evidence.

HOUSING

Housing Bust.

WSJ examines how interest rate hikes have threatened small investors that bought into real estate syndicators. High rents magnified by a boom in the rental market was a boon to them, who now hold properties they can’t afford. Industry analysts and investors foresee a coming wave of foreclosures. Flurries of syndicators now race to either sell or fundraise.

Congress in 2012 opened the door to the syndicators with a law that made it easier to market real-estate investments online. The law, intended to open financial opportunities to lower-income people, greatly expanded the reach and audience for syndicator deals. Syndicators largely favored apartment complexes in the South and Southwest, where real-estate prices were lower, rents were rising and housing regulations were generally looser. Many of these locales had fewer renter protections, which made it easier to evict tenants and raise rents.

Fannie and Freddie Fees.

Since the Federal Housing Finance Agency bumped up fees for higher-credit-score borrowers to offset fee slashes for their lower-credit-score counterparts, Republicans have moved to block the change. The Republican-led bill seeks not only to reverse the fee hike, but also prevent the FHFA from promulgating similar changes in the future.

Renters’ Paradise.

NYT takes the reader to Vienna, where social housing is inclusive and affordable. Here, 80% of Viennese qualify for public housing and contracts never expire, even if the resident’s income increases. And a little over 40% of all housing is “insulated from the market, meaning the rental prices reflect costs or rates set by law” and not subject to market fluctuations. The Austrian plan, the reporter writes, subsidizes construction – inherently increasing supply – while the American plan subsidizes people – with things like housing vouchers inherently increasing demand.

POLITICS and MONEY

Tim Scott.

The Senate Banking ranking member is putting in for the 2024 presidential election, starting out in the low single-digits in polling according to Politico. Scott is going up against DeSantis for the Republican primary. He enters the race with $22mn, more campaign dollars than any previous presidential candidate – to compare, Sanders came in with $14mn for the 2020 election.

Glenn Youngkin.

Virginia’s governor, who retired from the massive private equity firm Carlyle Group in 2020, is likewise considering a campaign for the Republican presidential nomination after previously dropping out. While the upcoming election is a possibility, a source close to Youngkin says it may just be a “dress rehearsal,” since 2024 would be his final year in the gubernatorial position.

Hi all! Remember to sign up for virtual scrimmages. Shawn is judging some of them and he's got two GPDA championships under his belt.. decentralized sports betting platform for crypto folks - https://tinyurl.com/3fbhv4ts