Stop Wall Street Looting – Act!

That’s what Senator Elizabeth Warren is hoping to do with the introduction of the Stop Wall Street Looting Act of 2024, or SWSLA (pronounced SWIZZ-lah if you’re cool). The bill is designed to close many of the legal loopholes the private equity industry has been able to exploit for decades to loot companies and create a new class of billionaires.

The private equity industry’s explosive growth over the past 20 years has damaged communities, consumers, workers, investors, the environment, and more. Just over the past year alone, private equity has offered up sobering case studies into how its business model wrings the life out of good businesses and leaves them injured or on life support. Like when a formerly PE-backed hospital system crashed and threatened to leave patients without care. Or like when it was revealed that the fossil fuel investments of just 21 firms pumped out more CO2e than every worldwide flight in a single year. Or like when a formerly PE-backed chemical plant blew up and spewed a toxic cloud of chlorine over Georgia. In all these cases, people were harmed while some already very rich people still managed to profit!

The list goes on, but your email inbox has a file size limit. Really, it would be easier to go over the industries that private equity hasn’t decimated.

SWSLA would make private equity firms and their executives responsible for the actions — and notably huge debt burdens — that harm a company and its workers, in some cases even after they no longer control it. Some additional elements include capping extractions like dividend payments at 10 percent of an acquired company’s overall debt for the duration of a private equity firm’s ownership. Another new provision extends the statute of limitations to examine potential fraudulent asset strippiing to 15 years, which provides an avenue to investigate private equity’s favorite cash-generating tactics.

Americans for Financial Reform applauded the introduction of the bill. Said AFR’s Lisa Donner:

“Private equity has an immense impact on the U.S. economy, touching virtually every aspect of life from healthcare to housing to technology to retail and more…Without major changes, a handful of ultra wealthy Wall Street executives will continue getting richer at everyone else’s expense. The Stop Wall Street Looting Act takes important, much-needed steps to rein in Wall Street predatory practices and promote a more just and sustainable economy.

While some lawmakers are aiming for reform, others (like vice presidential candidate J.D. Vance) have tens of millions invested in the private equity industry, with little in the way of disclosures. The Lever reports that ten senators and 16 representatives have more than $150 million invested in private equity, probably a significant undercount.

BANKING AND FINANCIAL STABILITY: Capital Requirements – Bank Mergers – The Law in Finance – Low Lending – A $3 Billion Settlement – Money Managers and Banks

CONSUMER: Coerced Debt – Arbitrary Arbitration – Why the Denial? – Unfair-way – Illegal Auto Practices – Risky Cash Fast – Absurd Percentage Rates – A Loan Shark in Your Pocket

CAPITAL MARKETS: Goldman Sachs

PRIVATE MARKETS: Big, Bad Deals – Is PE Out of Control? – Private Credit – A PE ETF – PE and Healthcare – Reaping What Others Sow – PE and Childcare – The Big Short? – And the Big Sports – The Highway to Hefty Costs

CRYPTO: The Crypto Kleptocracy – Stablecoins – FTX – Fakecoin – Crypto Lending – Crypto Sues the SEC – Community Bankers Fret About Stablecoins – High Speed Crypto

HOUSING: Tax Credits Expiring

CLIMATE AND FINANCE: The Global South – Lower Home Energy Costs – Manufactured Housing Insurance – Insurers Ensuring Climate Catastrophe – The Small Business Climate

POLITICS AND MONEY: Crypto Cash – Billionaire Oligarchs

Feedback? Reach us at afrnews@ourfinancialsecurity.org

BANKING AND FINANCIAL STABILITY

Capital Requirements.

The incoming slate of system-shoring Basel III Endgame capital requirements, which the bank lobby has pressured regulators into scaling back, isn’t strong enough, according to a group of economists. Using a dataset spanning 18 years, researchers at the Université Paris Ouest offer up evidence that the Basel III capital levels are set too low, noting that a lack of capital strength can often point to default risk.

Bank Mergers.

A new study by researchers at the University of Westminster found that U.S. bank mergers since the financial crisis are continuing to amass financial risks that can lead to “significant contagion.” The result of their study points to a significant increase in post-merger systemic risk, concentrated especially among larger banks that are now too-big-to-fail.

The Law in Finance.

Peter Conti-Brown, the esteemed historian and analyst of the Fed, has started a blog called PCB Central. (central banking, get it?!) One of his opening pieces: "Banks don’t historically sue their regulators. Is that about to change?" And his conclusion, following the Supreme Court’s overturning of the landmark Chevron decision, is sobering. In short, the Fed will get pushed around by the banks it is supposed to regulate:

I would wager that there will be a lot more litigation. And I would also wager that the Fed will sprint away from the courthouse door out of an overdeveloped fear that litigation will erode its independence. The last wager reflects a profound error on the part of the Fed ... The Fed’s fear of conflict is itself a political act.

Low Lending.

As they slog out of the Fed’s high-rate environment, U.S. banks are expected to report their lowest net interest income, which they earn from interest charged to borrowers, in almost two years. That’s still $62 billion, and it comes after a protracted boom in the very same net interest metric. Starting 2022, banks spent two years raking in $1.1 trillion in profits by earning more from loans than they paid in interest to depositors.

A $3 Billion Settlement.

In the largest ever combined penalty in anti-money-laundering enforcement, TD Bank will pay $3 billion in fines to settle charges for allegedly making it “convenient” for drug cartels and other illicit financiers to open accounts, transfer funds, and deposit seven-figure stacks of cash at its branches for over a decade. The penalty includes an asset cap of $370 million imposed by the OCC, the largest cap on big-bank growth since the Fed’s order on Wells Fargo’s in 2018.

Money Managers and Banks.

Asset mega-manager BlackRock controls more than 10 percent of about 40 banks, a level of ownership that can be considered a controlling stake – and one worthy of FDIC concern. An FDIC proposal, which has garnered support from Republicans and Democrats alike, could keep asset managers from holding too much sway over certain banks. The FDIC’s proposed rule poses important questions about how to deal with the outsized influence large asset managers like BlackRock and Vanguard have over banks on key issues like board composition, executive pay, and risks related to climate change, racial inequity, and lack of respect for labor rights. The FDIC just extended the comment deadline 30 days.

CONSUMER

Coerced Debt.

AFREF submitted a comment letter supporting a petition from the National Consumer Law Center and the Center for Survivor Agency and Justice asking the Consumer Financial Protection Bureau (CFPB) to provide relief to victims of coerced debt under the Fair Credit Reporting Act. The petition would provide critically needed relief to victims of coerced debt (a form of economic abuse) and further protect people who are survivors of intimate partner violence. Abusers commonly mislead their partners about loans, lie about paying bills, force their partners to share credit cards or co-sign for loans, and more as part of a strategy that undermines the financial stability of their victims and makes it harder to amass resources to seek safety and security. As AFREF noted, “the petition addresses significant barriers to financial inclusion for vulnerable survivors of intimate partner abuse, especially for women and people of color who are far more likely to face compromised credit scores from coerced debt that result from structural racial inequalities.”

Arbitrary Arbitration.

The CFPB found that the forced arbitration platform Ejudicate misled student borrowers about its neutrality in arbitration and illegally started sham forced proceedings against those borrowers with no opportunities even to consent to arbitration. A recent agency enforcement action against the company highlights an urgent need to curb forced arbitration, a practice that hurts millions of people and keeps misconduct hidden. Here, Ejudicate ran bogus arbitration proceedings on behalf of the predatory vocational software company Prehired, which was shut down by the CFPB and state attorneys general in 2023. Said AFR’s Christine Chen Zinner:

Forced arbitration clauses are a convenient corporate shortcut to hide misconduct that tricks people into giving up fundamental rights. Consumers need tough curbs on forced arbitration, not only in this instance, but across the board. This enforcement action reinforces the CFPB’s commitment to fair contract terms and a level playing field for consumers.

Speaking of forced arbitration: A case involving Uber exposed the harms of arbitration just last week. A New Jersey couple’s 12-year-old daughter was forced into clicking on a pop-up box to track her Uber Eats pizza. Little did she know that she had just agreed to forced arbitration. One year later, her parents were seriously injured when their Uber driver ran a red light and T-boned another vehicle. A New Jersey court ruled that the couple could not hold Uber liable in court because the pop-up their daughter had apparently agreed to — as Chen Zinner explains — waived their right to a trial by jury.

Why the Denial?

AFREF submitted a comment to support the National Consumer Law Center's petition urging the CFPB to narrowly define residential real estate leases as “credit” and landlords as “creditors” under the Equal Credit Opportunity Act to require landlords to disclose why they rejected rental applicants and to prevent the consideration of medical debt on credit reports in tenant screening.

This petition for rulemaking addresses important components of the ongoing legacy of structural racism in credit and residential housing for people of color seeking rental leases to shelter their families and build a foundation for economic stability.

Unfair-way.

The CFPB and Department of Justice has slammed a top mortgage lender, Fairway, with a $1.9 million penalty for illegal redlining against majority-Black neighborhoods in Birmingham, Alabama. The two agencies allege that the company, through its marketing and sales tactics, discouraged people from taking out mortgages in Birmingham’s Black neighborhoods. On top of the penalty, the company will also be required to provide $7 million in a loan subsidy program to “offer affordable home purchase, refinance, and home improvement loans in majority-Black neighborhoods.”

Illegal Auto Practices.

Sometimes, auto lenders take you for a ride. In a supervisory report, the CFPB scrutinized detailed data on auto repossession and lending, revealing that many Americans deal with “unnecessary costs and challenges paying for their car.”

Auto finance companies, especially those targeting consumers with subprime credit scores, often offered superfluous add-on products (like extended warranties or guaranteed asset protection insurance) and even charged for optional add-ons to which consumers didn’t consent. Other lenders improperly applied payments and prevented borrowers from making progress toward paying down the principal and interest charges, resulting in wrongful repossession. Sometimes, lenders provided inaccurate disclosures and sent false information to credit reporting agencies.

Risky Cash Fast.

Looking for fast cash? A payday loan might seem tempting, but think twice, the FTC suggests! While it offers quick relief, the steep fees and sky-high interest rates can leave you trapped in a cycle of debt. Rollover fees and high interest could add up to more than the original borrowed amount. Before committing to a payday loan, consider cheaper alternatives like asking for an extension, borrowing from friends, or exploring low-interest options from credit unions.

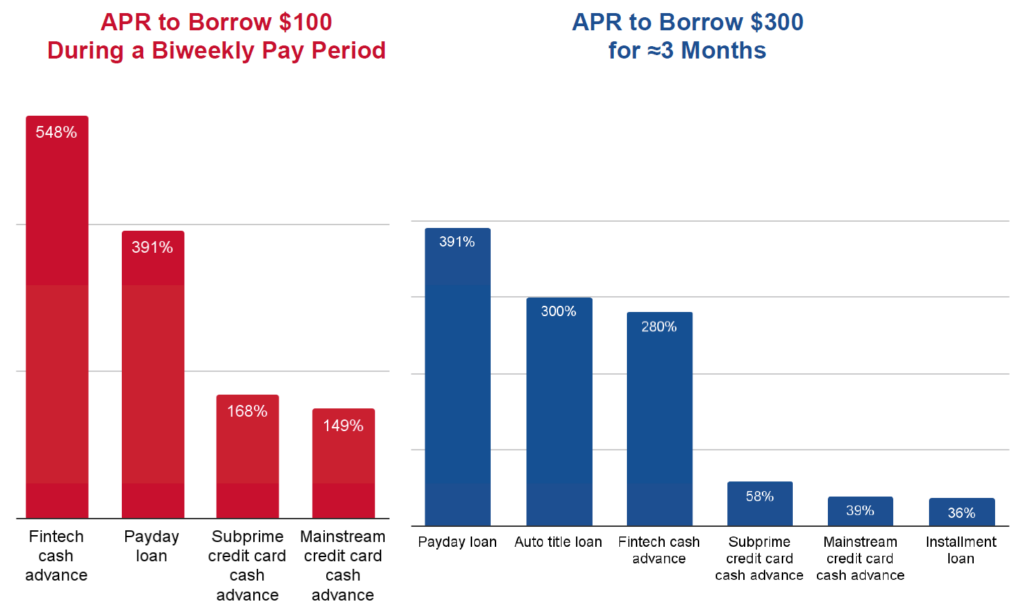

Absurd Percentage Rates.

The National Consumer Law Center compared the annual percentage rates (APRs) of different types of small-dollar loans and found that several high-cost options – like fintech cash advances, payday loans and other options, had triple-digit APRs compared to slightly longer-term loans made on mainstream credit cards or in installments.

Chart by the National Consumer Law Center.

A Loan Shark in Your Pocket.

That’s what the Center for Responsible Lending (CRL) calls earned wage advance (EWA) offerings, third-party apps that allow workers to access their paychecks early if they pay piled-on charges. Cash advance apps can slam consumers with what amounts to exorbitant, triple-digit interest rates through fees. Many cash advance borrowers are trapped in a debt cycle, and use of these apps is associated with overdraft fees and payday loan use, CRL’s report finds.

CAPITAL MARKETS

Goldman Sachs.

The megabank made $3 billion in profit in Q3 2024, owing to an increase in its stock trading business even as it scaled back its consumer banking.

PRIVATE MARKETS

Big, Bad Deals.

KKR is under fire by the Department of Justice (DOJ) for allegedly withholding information about the competitive impact of its merger and acquisition activity from government inquiries. The DOJ has two ongoing investigations into KKR, one civil and one criminal. The agency is pursuing a $100 million penalty and an agreement that the firm’s co-chief executives sign off on pre-merger review filings, effectively making KKR’s top dogs personally liable for future shortcomings. AFREF has supported the DOJ and Federal Trade Commission efforts to more strongly enforce antitrust rules against private equity roll-ups where private equity firms skirt merger review by making a series of smaller takeovers to build a bigger monopolistic portfolio company.

The increased pressure on firms to comply with antitrust laws comes at a time when PE firms were responsible for at least 40% of all M&A activity, according to 2022 numbers. Incoming pre-merger notification rules, though lightened from their original form, would increase transparency and help to better detect anticompetitive combinations.

Is PE Out of Control?

The Guardian takes a deep dive into private equity and finds the metaphor of a virus works well in explaining the financial world’s supervillains:

A coronavirus replicates by injecting its RNA into the cells of a target organism. Once inside, the RNA hijacks its host’s resources to build more copies of the virus, weakening and sometimes destroying the host in the process. Private equity’s business model is similar … We’re letting it take over our cells and replicate aggressively. It’s clear who’s on the winning side of that bargain.

Private Credit.

Some megabanks, like JP Morgan, are dipping deeper into private credit — the opaque corner of private lending that can amplify potential systemic risk — as the volume of this private lending and debt load mounts. Private lenders have allowed a growing number of companies to avoid making interest payments using what is called “payment-in-kind” arrangements, in which companies struggling to pay down their debts can defer payments… by taking on more debt. Exposure to private credit has grown among banks.

A PE ETF.

The Consumer Federation of America warned the Securities and Exchange Commission about the launch of a private credit exchange traded fund (ETF) from State Street which uses assets sourced by private equity megafirm Apollo. CFA is concerned the proposed ETF does not comply with the Investment Company Act and its rules relating to liquidity, valuation, and conflicts of interest. This comes as private equity is sitting on over $3 trillion in assets they are struggling to sell and their existing investors have been investing less in their new funds as they grow impatient waiting to get their money back from the existing private equity investments. These private equity ETFs are a way to push private equity onto retail investors who may not understand the risks of private equity.

PE and Healthcare.

Private equity’s predatory strategies are on full display in the Healthcare sector. Goldner Capital Management, once a major player in nursing homes, is bankrupt, with its CEO blaming a deceptive COVID-era lending scheme. Meanwhile, Steward Health Care was drained dry by private equity firm Cerberus and Medical Properties Trust (MPT), which bled the hospital chain with inflated leases and hidden debt.

Reaping What Others Sow.

Private equity is sampling Napa Valley’s finest with Butterfly Equity’s $2 billion purchase of Buckhorn portfolio, financed through a handful of farm banks in the U.S. Farm Credit System. The luxury wine producer has faced stagnating sales thanks to a recent big acquisition and lack of youth interest in wine.

PE and Childcare.

Private equity firms have rapidly expanded into the U.S. child care industry, with private equity-backed chains now managing an estimated 10 percent of child care services. This expansion raises concerns about PE profits and predatory practices undermining the quality of care as well as the potential collapse of a major provider, triggering a child care crisis. The pressure from profit-driven and debt-loaded models could lead to lower quality care and financial instability, much like when Australia's ABC Learning chain collapsed in 2008 and caused a childcare crisis so large that the government had to intervene and convert the chain into a nonprofit.

The Big Short?

Private equity firms are having trouble getting out of their investments. Jared Dillian, a financial author who penned the report The Next Big Short: Hidden Risks Behind Private Equity’s $8 Trillion Market, explains that the problem could get out of hand fast:

Here’s the systemic risk, here’s the problem. So a stock market decline doesn’t last very long. Like even the financial crisis happened very quickly. But if you have 17,000 private equity firms liquidating their portfolios of companies over a period of five to 10 years, then it’s going to result in depressed valuations for a very long time.

The ill omen comes at a time when PE-backed firms are defaulting at higher rates, and any acquisitions that are going through have become less valuable to the firms.

And the Big Sports.

The Big Ten and the Southeastern Conference, two of the largest and wealthiest athletic conferences in college football, met to form a “united front against private equity.” Any changes related to PE stakes in college teams are unlikely to pass without the support of these two influential fronts, ESPN writes.

The Highway to Hefty Costs.

The state of Texas is buying back one of its highways from private equity – and it’s using taxpayer dollars to do it. In 2015, Texas Transportation Commission entered into a 52-year contract with the Blueridge Transportation Group (BTG) that allowed the consortium of six equity partners to build and operate a 10-mile stretch of private toll road built in the median strip of a public highway. In 2023, private equity firm ACS Group bought out its partners, then “operated the tollway like most private equity firms operate any company: invest a scant amount, accumulate debts, and siphon as much profit as possible before getting out without assuming liability for the company’s long-term debt.” Now, Texas has taken out a $1.7 billion loan to buy it out, and the state plans to recoup the losses with toll revenue from drivers.

CRYPTO

The Crypto Kleptocracy.

Crypto is rife with scams, hustles, cyber-breaches, rip-offs and rug-pulls. AFR’s Mark Hays talks about just a few of the ways that bad actors manipulate the crypto space: hackers often exploit coding flaws of decentralized finance, scammers run rug-pulls on unsuspecting victims, and phishing and access control attacks happen frequently. Hackers have been known to manipulate oracles — programs that provide external price data — to feed fake info and trick them into making bad trades. Money laundering using crypto is also rampant, offering criminals anonymity and portability.

Related: AFR’s Iván Cazarin lowlights how con artists are increasingly turning to crypto in scams that target older people. Cazarin estimates there were likely 750,000 crimes against older people involving crypto in 2023.

Stablecoins.

Treasury Secretary Yellen says that legislation being workshopped in Congress “comes close” to the Biden administration’s goals for stablecoin regulation, noting the risks that the crypto assets — which are typically pegged to the value of an outside asset or fiat currency — pose to financial stability.

FTX.

FTX’s bankruptcy plan promises to pay back 98 percent of the money it siphoned from its customers within 60 days. But those expecting a payout based on crypto’s rebound value since 2022 are getting the short end of the stick. Despite some prices having tripled over the last two years, the exchange claims to repay only 118 percent to their customers.

Fakecoin.

Eighteen fraudsters have been caught in the FBI’s net and are being charged with market manipulation and wash trading. The FBI’s crypto enforcement effort, Operation Token Mirrors, created a fake token (NexFundAI), which attracted crypto services that allegedly specialized in inflating trading volumes and prices for profit. The FBI then found that the defendants were involved in a sophisticated fraud that manipulated the values of over 60 tokens. Authorities have seized more than $25 million in crypto and deactivated multiple trading bots responsible for millions in wash trades. Several of the defendants have already pleaded guilty.

Crypto Lending.

The crypto company Tether, issuer of the world’s largest stablecoin USDT, is acting like a shadow bank as it explores plans to lend to commodities traders, an industry that typically leans on traditional banks for credit. Bloomberg flags that Tether’s funding line wouldn’t be subject to the same legal oversight as traditional lenders, a phenomenon known as regulatory arbitrage.

Crypto Sues the SEC.

After receiving a Wells notice (effectively a notice that the SEC plans to bring an enforcement action), the crypto trading platform Crypto.com sued the SEC over what it views as a government overreach. AFR has long advocated for affirming the SEC’s primary regulatory authority to regulate crypto industry actors, since many crypto products and services function like securities.

Community Bankers Fret About Stablecoins.

Bank lobby groups have been at times quiet about the march of crypto legislation — until now. The Independent Community Bankers of America, a powerful bank trade group, has now weighed in forcefully with concerns about stablecoin legislation that might be on the table in the lame-duck session of Congress this year. In Independent Banker, it writes of the "outsized risks that stablecoins pose to consumers and the financial system," the danger of breaching the wall between finance and commerce, and more.

High Speed Crypto.

The SEC sued the crypto arm of the high-speed trading firm DRW Holdings for its alleged failure to register as a securities dealer. It’s a meaningful move in the fight for crypto reform, since the agency is going after a business that “trades with hedge funds and other big market players,” writes the Wall Street Journal.

HOUSING

Tax Credits Expiring.

The federal Low-Income Housing Tax Credit finances the majority of affordable housing construction in the United States. Unfortunately, the Reagan-era tax credit program was designed with a major flaw: credits expire after 30 years. With the credits’ expiration on the horizon for affordable housing across the country and no federal obligation to keep the buildings affordable, many landlords have taken to a rent-hiking frenzy. For thousands of families, it could mean eviction. State housing finance agencies can impose additional affordability requirements and tenant organizations are trying to keep housing affordable, but there’s limited data on their success — or failure.

CLIMATE and FINANCE

The Global South.

A new report from AFREF, Consequences of U.S. Climate Financial Regulation and Investment on the Global South, scrutinizes how U.S.-regulated institutions have caused harmful climate impacts in the Global South – comprising many countries that contribute the least to global climate change but suffer most – and calls on policymakers to play an active role in addressing the challenges. The report recommends financial and trade reforms to enhance accountability, inclusivity, and transparency of financial flows toward countries in the Global South and to spur equitable and just climate investment. Said AFR’s Alex Martin:

“The best way to mitigate climate-related financial risks in an equitable and just way is to take into consideration the voices of a wide range of stakeholders in the Global South about what they actually need to execute a just climate transition.”

Lower Home Energy Costs.

Since 2023, AFREF and partners have been part of the Campaign for Lower Home Energy Costs, an initiative to get the FHFA to require new homes with mortgages backed by Fannie Mae and Freddie Mac (government-sponsored enterprises) to be built to modern energy codes. In April 2024, HUD and USDA announced the adoption of minimum energy standards for new single- and multi-family homes. In May 2024, AFREF organized a letter to the FHFA to adopt energy efficiency standards. And in June 2024, over 5,600 supporters called on the FHFA to follow HUD and USDA’s leadership.

Manufactured Housing Insurance.

Residents of Ocean City, Maryland, are struggling as insurance companies drop coverage on decades-old manufactured homes. The result is more than half of the Montego Bay community’s 1,523 properties are left with disrupted coverage. The lack of insurance has halted real estate transactions, forcing cash-only sales and self-insurance requirements.

This issue reflects a broader trend seen in high-risk areas across the United States, as insurers raise premiums or completely drop policies. Homeowners are left with few options and little to no government assistance, exacerbating financial strain in increasingly vulnerable areas.

Insurers Ensuring Climate Catastrophe.

Rest assured, insurers will save themselves before ever trying to save the people whose homes are devastated by climate-intensified natural disasters. That’s the central idea of an op-ed by the Climate and Community Institute’s Moira Bliss, who criticizes insurance companies’ refusal to renew policies, coverage scalebacks and complete retreat from certain areas. Bliss writes:

Take for instance insurers’ earnings on investment income (which includes fossil fuel investments, the top driver of climate change) or the hedging insurers do using tools like reinsurance (insurance for insurers) and financialised products like catastrophe bonds. Omitting these factors sidesteps how insurers still enjoy record share prices and profits while homeowners suffer.

Speaking of insurance companies investing in fossil fuels: Green America has a Climate Smart Insurance Directory that provides alternatives to the super-big insurance companies that underwrite fossil fuels.

Places like New York City are feeling the pressure too, as homeowners in the city stare down higher insurance prices and cut coverage. AFR’s Caroline Nagy flags climate change and inflation both are raising insurance costs: “Housing is a lot more expensive than it used to be, so the value of it is higher, and that means it’ll cost more to rebuild.”

The Small Business Climate.

In a survey of over 500 small business owners conducted by Small Business for America’s Future, entrepreneurs across the country say that climate-related events could have a “significant financial impact on their operations,” which may lead to increased prices for consumers. Over half of small businesses have already incurred climate-related expenses, like higher insurance premiums, higher energy costs, or business disruptions.

POLITICS and MONEY

Crypto Cash.

Crypto billionaires are flooding Ohio’s Senate race with millions of dollars in an attempt to unseat crypto skeptic Sen. Sherrod Brown. If they’re successful, The Intercept writes, “it could lead to more success for an agenda that includes neutering the Securities and Exchange Commission and opening the door for more traditional banks to hold crypto,” among other measures that would endanger investors, consumers, and the broader financial system.

Billionaire Oligarchs.

The New Yorker has a long read on the billionaires who are supporting Trump, and a good portion of them made their money on Wall Street. And even by the standards of rich Americans, their desire to run the country over the objections of the rest of us stands out:

Trump’s billionaires—many of whom have made their fortunes as hedge-fund managers, activist investors, and corporate raiders—tend to be highly motivated ideologues and individual operators. “It’s transactional, but their end of the bargain is a lot different than just having access to the President of the United States,” [Princeton historian Sean] Wilentz told me. “They see Trump as their instrument. This is an investment for them to take power.” Wilentz noted that, unlike the “traditional corporate conservative élite” dating back to the Gilded Age, this new “class of the super-rich” appears both more numerous and less civic-minded. “The other guys might have been robber barons,” Wilentz said. “These guys are oligarchs.”

Thank you for keeping us informed!