Private Equity Plays with Your Life (Insurance)

Life insurance helps a family manage their financial life after someone dies. It’s a big thing to think about with big implications for some indistinct future beyond them. But to private equity, your life insurance is just a piggy bank they dip into to fund their business — family wealth and security be damned.

A new report from AFR examines that Risky Business: Private Equity’s Life Insurance Gambit. PE firms control $774 billion in insurance company assets, turning that cash into the fuel for leveraged buyouts and private credit arrangements. While insurers have always generated profits by investing the premiums they reap from policyholders, ownership by private equity has pushed many of those investments into riskier bets, like collateralized loan obligations. Sometimes, insurers, like some of those backed by the firm Eli Global, fail when they’re unable to cover their policy obligations.

Says AFR’s Andrew Park:

“Private equity owners on Wall Street are forcing far more risk onto life insurance companies than they have assumed in the past, with potentially perilous implications for policyholders, investors, and financial stability.”

Recently, the Financial Stability Oversight Council (FSOC) and International Monetary Fund (IMF) both scrutinized how private equity’s interest in insurers may damage financial stability. PE’s tendency to put insurers’ investments in complex assets “elevates liquidity and complexity risk and raises questions about the quality of assets,” FSOC said in its report. Said AFR’s Patrick Woodall: “The increased scrutiny is a recognition that private equity-owned insurers pose risks not just to policyholders, but to the broader financial system.”

AFR’s report recommends enhanced attention from FSOC and designation of insurers as Systemically Important Financial Institutions, improved oversight from state officials, and better federal oversight of leveraged loans and the rapidly growing private credit market.

FINANCIAL STABILITY: Backstop Demand – Banks and Nonbanks – Small Lender Turbulence – Fallacies of Financial Innovation – Financial Data Collection – Further to the Banking Crisis

CONSUMER: Forced Arbitration – Student Loans – Overdraft – Credit Card Late Fees – Enforcement Actions

CAPITAL MARKETS: Enforcement Efficacy – Stock Buybacks

PRIVATE MARKETS: Private Equity in Healthcare – Pensions, Politics, Private Equity – Private Credit – Other Private Markets News

CRYPTO: Stablecoin Securities – A Bitcoin ETF? – A Crypto Exec Who Doesn’t Exist

HOUSING: An “Extinction-Level Event” for REALTORS® – Built to Rent – Florida Insurance

Feedback? Reach us at afrnews@ourfinancialsecurity.org

FINANCIAL STABILITY

Backstop Demand.

The week through Dec. 20 saw a record amount of borrowing by banks from the Bank Term Funding Program, the backstop facility created during this year’s banking instability that allows “banks and credit unions to borrow funds for up to one year, pledging US Treasuries and agency debt as collateral valued at par,” Bloomberg explains. Over the course of the week, the BTFP lent $131bn, with more borrowing institutions turning to the Program instead of the discount window. It’s a risk-free bet underwritten by the Fed, per Bloomberg: “institutions borrow from the facility before parking the proceeds in their accounts at the Fed to earn interest on reserve balances.”

Banks and Nonbanks.

The Fed, FDIC and OCC want to revise the information banks publicize on their call reports. Among the changes, regulators want to know, as Bank Reg Blog outlines, how much traditional banks lend to nonbanks, such as “insurance companies, mortgage companies, private equity funds, hedge funds, broker-dealers, [REITs], marketplace lenders, special purpose entities, and other financial vehicles.” Regulators report that in June 2023, loans made to these nonbanks rose to $786bn, up from $56bn in 2010, representing 6.4% of respondents’ loan exposure.

Small Lender Turbulence.

The high-rate environment that helped sink several midsize lenders earlier this year continues to batter the community lenders that “fuel local economies” with smaller, more local loans. Deposits climbed post-pandemic, but low interest rates meant low loan growth. To make up for it, banks pushed their deposits into Treasurys, mortgage-backed securities and bonds. Then, as the Fed cranked interest rates higher, those investments began to devalue. One bank profiled by WSJ, Texas-based Industry Bancshares which has about $5bn in assets, is over $75mn “underwater” and its liabilities have outpaced its assets since 2022. Now, it’s considering changes that may result in merging some of its branches – drying up credit access in communities – or selling off deposits.

Fallacies of Financial Innovation.

Prof. Saule Omarova tackles three myths that “invisibly shape and quietly distort the ongoing debate on pros and cons of financial innovation” in a new paper. Myth #1 is the most potent one, about how Wall Street cultivates the false impression that most of what it does involves raising capital for productive purposes. In fact, much of what Wall Street does is pure speculation.

Financial Data Collection.

The Brookings Institution’s Aaron Klein summarizes six major themes from an event about bolstering financial data collection efforts. Among them: Office of Financial Research, resilience issues, and climate risks

Further to the Banking Crisis.

Signature Bank. The FDIC has sold a 20% equity interest in a $9bn parcel of rent-stabilized multifamily loans to an entity owned by midsize lender Santander Bank for a sum of $1.1bn, days after it closed on a similar deal with a Blackstone-affiliated entity for commercial real estate loans.

What’s Happening to Banks? A Bloomberg op-ed from former NY Fed president says the Fed is “still keeping the public in the dark about the deficiencies it finds at US lenders” and calls for “well-placed transparency.” While securities laws require banks to disclose supervisory issues, regulators keep it confidential, often leading to regulatory action (merger cancellations and prohibited expansion, for example) that occurs without a nod to the “underlying reason.”

CONSUMER

Forced Arbitration.

When a company forces a consumer into arbitration in response to a grievance, that consumer (sometimes an employee in an internal case) often waives their right to pursue the matter in a civil court or as part of a class action. Instead, they’re at the mercy of a behind-closed-doors, binding adjudication process headed up by the offending company.

New research indicates that these number of cases ballooned by 467% in 2022, but consumers/employees came out the winner only 0.7% of the time. In 2022, however, consumers increasingly fought back with mass arbitration – a large number of “individual claims filed at the same time,” though win rates were still rock-bottom. Corporations’ arbitration strategies have evolved, at a detriment to the consumer, to force arbitration without an agreement, make it more difficult for offended parties to win, refuse to pay fees, and group claims together to dismiss them all at once. Fintechs, like Buy Now Pay Later player Klarna and digital payments platform Zelle, have also come under fire for their arbitration practices.

This week, a group of law professors spoke out against forced arbitration in an op-ed for The Baltimore Sun. They, along with 160 other professors late last year, urged the CFPB to protect consumers from “fine print traps.”

Student Loans.

A report from the CFPB highlights several challenges borrowers face as student loan repayments resume. The major findings:

Customer Service. Many borrowers have to wait on hold for more than an hour when they call their servicer, many of them abandoning their place in line without ever receiving assistance. During the pandemic, many companies reduced staffing to improve financial performance, but rehiring hasn’t kept up with demand.

Delays. By October, 1.25mn applications for income-driven repayment remained pending. 450,000 were pending for over a month with no resolution.

Inaccuracies. Borrowers are receiving “fault and confusing bills” that include premature due dates, inflated monthly payments using outdated guidelines, and the use of incorrect income to determine new payments.

Overdraft.

Despite a survey from the CFPB finding consumers still struggle with excess overdraft fees and an Accountable.US survey highlighting the popularity of a crackdown on junk fees, the bank lobby has launched a “smear campaign” against an as-yet-unreleased rule that would limit overdraft fees and save consumers billions. In a letter, the American Bankers Association, America’s Credit Unions and Independent Community Bankers of America argued the rule would be too onerous for smaller institutions.

Credit Card Late Fees.

The CFPB has worked to lower the cap on credit card late fees from its current maximum of $41 to $8, seeking to save consumers billions every year. The American Economic Liberties Project provides an overview of the issue here. Americans with lower credit scores are “much more likely to pay repeat late fees,” with those under 580 paying $138 on average in 2019 compared to $11 among those with a score of 720 or higher. This, AELP writes, makes late fees “essentially a poor tax, preying on low-income Americans.” AFR and other organizations have called on the CFPB to finalize its rule.

Enforcement Actions.

Colony Ridge. The Texas-based lender faces a suit from the CFPB and Department of Justice for “operating an illegal land sales scheme and targeting tens of thousands of Hispanic borrowers with false statements and predatory loans.” The company sold families “flood-prone land without water, sewer, or electrical infrastructure,” then saddled them with loans they couldn’t afford. About a quarter of their loans end in foreclosure.

Manchester City Nissan. The FTC and State of Connecticut issued a complaint against the auto dealer for “systemically deceiving consumers about the price of certified used cars, add-ons, and government fees,” charging them junk fees for certain services and add-ons without consent.

CAPITAL MARKETS

Enforcement Efficacy.

The SEC’s enforcement has led to positive changes in behavior, reports SEC enforcement chief Gurbir Grewal in an interview with WSJ. The year through September 30 saw the SEC levy $5bn in financial remedy through 784 enforcement actions.

Stock Buybacks.

The SEC is “poised to rework” its stock buyback rule after it was struck down by the conservative-dominated Fifth Circuit Court of Appeals. The rule would have strengthened the disclosure guidelines for companies performing repurchases (buying back their own stock to take shares out of circulation) and required them to provide the rationale for these buybacks, in the interest of arming investors with information. AFR previously called on the SEC to re-propose after industry-led attacks on “basic transparency.”

PRIVATE MARKETS

Private Equity in Healthcare.

The short of it: private equity involvement in medicine makes healthcare worse.

First, hurting in hospitals: A study published late last month in JAMA revealed, in an analysis of about 4.5mn hospitalizations, that private equity-owned hospitals were associated with higher incidence of “hospital-acquired adverse events” than their non-PE-owned counterparts. Despite generally receiving lower-risk patients, care centers that had been acquired by private equity firms saw 25.4% higher rates of events like falls or bloodstream infections from central lines between 2009 and 2019.

Second, wringing out nursing homes for cash: “Private equity firms and their affiliated lenders, in the pursuit of profit in America’s growing nursing home industry, are speculating in a way most traditional banks will not,” Politico reports.

Third, defaults: Many healthcare companies are overleveraged and under-liquid, leading to a rise in defaults with more to follow in 2024. Some of the providers which had their credit rating downgraded to default this year were owned by private equity, such as Envision (KKR) and Air Methods (American Securities).

So, why are doctors selling to private equity? An op-ed in the Hill explains that while regulators do need to take steps to address ownership by private equity firms, physicians sell to PE because it often presents itself as the most appealing, most lucrative option. The foremost reasons a doctor goes through with any such deal are to secure higher reimbursement rates from insurers, which they can’t negotiate on their own, and to tap into more capital to cover rising costs.

Pensions, Politics, Private Equity.

A paper from the University of Illinois’ Jaejin Lee determines that when private equity general partners (GPs) make donations to candidates that go on to win their state election, that state’s public pension fund becomes more likely to make private equity allocations. “These connected pension funds pay higher PE fees and exhibit more home-state bias, suggesting politicians influence investment decisions for personal gain,” Lee writes.

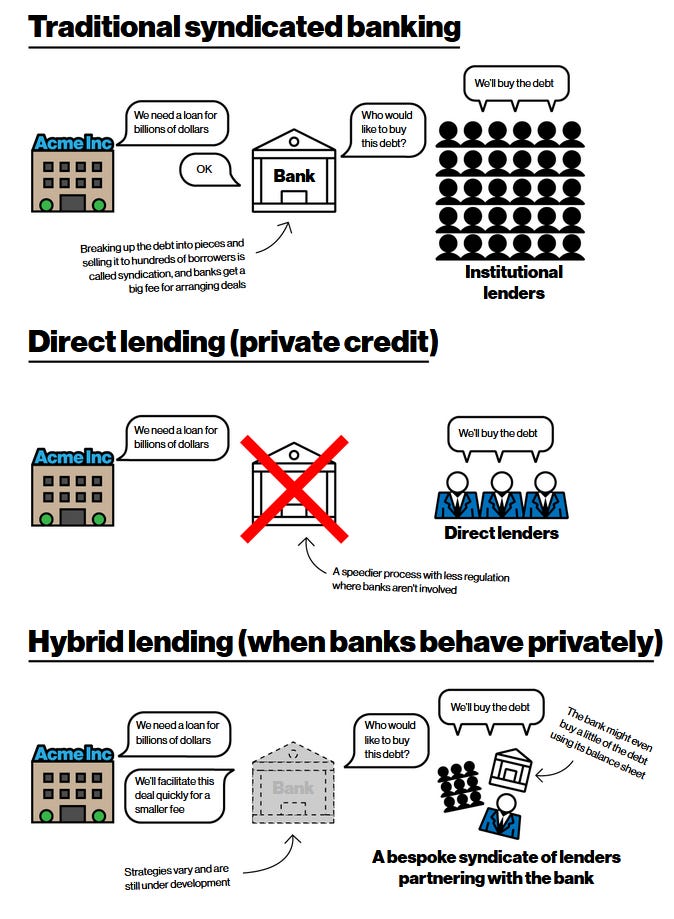

Private Credit.

Bloomberg explains private credit and why banks want a piece of the action. Lately, nonbanks have gained ground “in the business of providing debt to risky companies,” providing big money to big deals. Traditional lenders, like JPMorgan Chase, have stepped into the fray: “The model they’re using, when stripped down to its most fundamental elements, looks strikingly similar to their vaunted leveraged lending outfits. Hamstrung by regulatory constraints that limit how much of their own capital they can put on the line for long periods of time, they’re leaning on their extensive network of corporate clients to drum up deals, pairing with deep-pocketed investors for financing, and looking to reap juicy fees from acting as go-betweens.”

Other Private Markets News.

Greyhound. The intercity bus company has been selling off terminals, and private investors have been cashing in. The hedge fund Alden Global Capital has been quick to sell the depots they purchase to real estate developers, effectively accelerating their closures. As stations continue to shutter their doors, the impact falls disproportionately on minorities, people with disabilities and the unemployed, many of whom would not be able to make their trips without these bus lines.

Skiing. Private equity has cut into snowsports too. PE acquisition of ski resorts has led to a duopoly dominated by two companies, Ikon Pass and Epic Pass. Workers have suffered as some resorts, for example, have failed to compensate workers for breaks, meetings, trainings and gear. And the pastime’s become more expensive to the average enthusiast.

Activity. Between 2022 and 2023, private equity M&A activity declined by about 40%, strained by high interest rates, difficulties in exits and a pullback by investors, WSJ reports. As a consequence, “money being returned to pension funds has ‘fallen off a cliff’.” And buyout firms want out of some of the unsold $2.8trn in investments they have made to put a $2.59trn reserve of cash to work.

CRYPTO

Stablecoin Securities.

Federal judge Jed Rakoff ruled that the stablecoin Terra, and other tokens offered by the failed Terraform Labs, is a security in what’s been considered a win for the SEC. Some context: One of the (many) tensions in crypto regulation has been whether tokens are classified as securities or commodities, as it has an effect on how they’re treated and which agency oversees them. Previously, a different federal judge in a separate case about Ripple Labs’ XRP token classed it as a security sometimes (when bought by institutional traders) and not in other times. Rakoff’s ruling is a departure from that interpretation, and means Terraform’s tokens are unregistered securities.

A Bitcoin ETF?

The SEC appears likely to approve the first-ever Bitcoin ETF, launched by major asset managers. Politico expects it to “become another front in Washington’s crypto clashes, fanning long-running debates over the market’s value and riskiness for everyday investors and retirees.”

A Crypto Exec Who Doesn’t Exist.

Thousands of people lost millions of dollars after being convinced to invest in an Australian crypto scheme called HyperVerse, which amounted to a “suspected pyramid scheme” and has since collapsed. At a launch event in 2021, the fund introduced someone named Steve Reece Lewis as HyperVerse’s CEO, assigning him a glittering career summary that took him from the University of Cambridge to Goldman Sachs, and beyond. The problem: nobody named Steven Reece Lewis exists in the record in any of the sectors with which he was associated. Lewis’ Twitter account had only existed a month before he appeared in the launch video. And The Guardian couldn’t find any evidence about his identity.

HOUSING

An “Extinction-Level Event” for REALTORS®.

Late December, the real estate marketplace Zillow sued numerous listing services across the United States, “accusing them of forcing Zillow’s listing service out to maintain illegal monopolies.” Several property listing services, many of which are affiliated with the National Association of Realtors trade association, allegedly phased out Zillow’s services from their platforms. Taken together with a decision in October requiring NAR to award $1.8bn to homesellers for having artificially inflated prices, sexual harassment allegations against leadership, major brokerages no longer requiring their agents to maintain NAR memberships, and a Justice Department investigation for antitrust violations, the organization fears an “extinction-level event” that could take the 1.5 million-member trade group out of commission.

Built to Rent.

Wherever Wall Street investors can’t buy properties in the neighborhoods they want, they’ll just build their own communities “where every detail has been designed to keep costs down” for their landlords. These institutional investors, who already own over half of all apartment units in the country, have long eyed single-family homes as lucrative rent-farms. But during Q3 2023, big landlords represented about 1% of home sales, compared to 3% throughout 2022. Instead, corporate landlords are creating build-to-rent communities, where homes might, for instance, “have a wide hallway and stairs to protect the paintwork” and keep maintenance costs for landlords low.

Florida Insurance.

Amidst a growing insurance crisis in Florida, whose climate-ravaged homes are losing affordable coverage, some insurance companies are able to employ a “takeout” to scoop up thousands of policies at once without acquisition costs. Then, they’ll “cherry-pick” the most lucrative policies to underwrite and leave the least lucrative high and dry. While insurance executives benefit, the practice “has been crippling many residents and disaster victims, who are paying some of the highest prices in the nations for insurance while experiencing some of the worst claims handling and processing times,” WashPost reports.