CFPB Creaks Back to Life as Resistance Mounts

The Consumer Financial Protection Bureau (CFPB), despite the Trump-Musk onslaught, is showing signs of a revival.

After weeks of court battles and employee purges, the lights are flickering back on—literally. The front page of the agency’s website, which read “404” the day Trump officials stormed in, is functioning again. But behind its partial resurrection lies a deeper crisis: an orchestrated campaign to gut the only federal consumer watchdogs solely for financial services.

The agency’s battered staff continues to work as best it can. The consumer response team was just called back to tackle 16,000 unresolved complaints, including dozens from families on the brink of foreclosure. The Fair Lending Office is preparing its annual report to Congress.

Don’t be fooled by Wall Street spin or Trump-aligned talking points. Voters overwhelmingly support the CFPB. But, since taking over, the Trump-appointed CFPB leadership has slashed 17 percent of its staff and even drafted plans to fire 1,175 employees. In blatant defiance of the courts, the agency continued termination meetings after injunctions were issued.

With the CFPB in chaos, consumers are left vulnerable. Payday lenders, predatory mortgage firms, and debt collectors stand to benefit as financial protections erode. The shutdown of enforcement actions means military families, struggling borrowers, and everyday people lose critical safeguards against fraud and financial abuse.

For a sense of what a world with no CFPB was like for one consumer, check out this video about a man in Virginia whom the agency was helping to wrangle $45,000 back from PayPal. But when CFPB was off the job, PayPal ignored him.

During a House recess, people are making their voices heard back home—through town halls, rallies, and op-eds. Across the country, constituents are calling on their representatives to protect the CFPB and the critical safeguards it provides.

In Colorado, Greeley Tribune published an op-ed from Bethany Pray at the Colorado Center on Law and Policy urging Rep. Gabe Evans to stand up for working families by defending the CFPB.

New Jersey Citizen Action called on the state’s lawmakers to do their part: “The New Jersey delegation in Congress must stand up for their constituents against the Trump administration and DOGE, his big-business protection arm.”

In New York, local media reported on the dangers of rolling back the CFPB’s caps on overdraft fees.

A letter-writer in Victoria, Texas said simply: “Leave the CFPB alone.”

The Kiowa County (Colorado) Press highlighted how cuts to the CFPB put Coloradans at risk of exploitation by predatory lenders.

A New Jersey manufactured home owner urged other people who rely on this affordable form of housing to contact members of Congress and urge them to support the CFPB.

In the Lehigh Valley State Ledger, Pennsylvania State Senator Lisa Boscola emphasized the CFPB’s success in shielding families from unfair business practices.

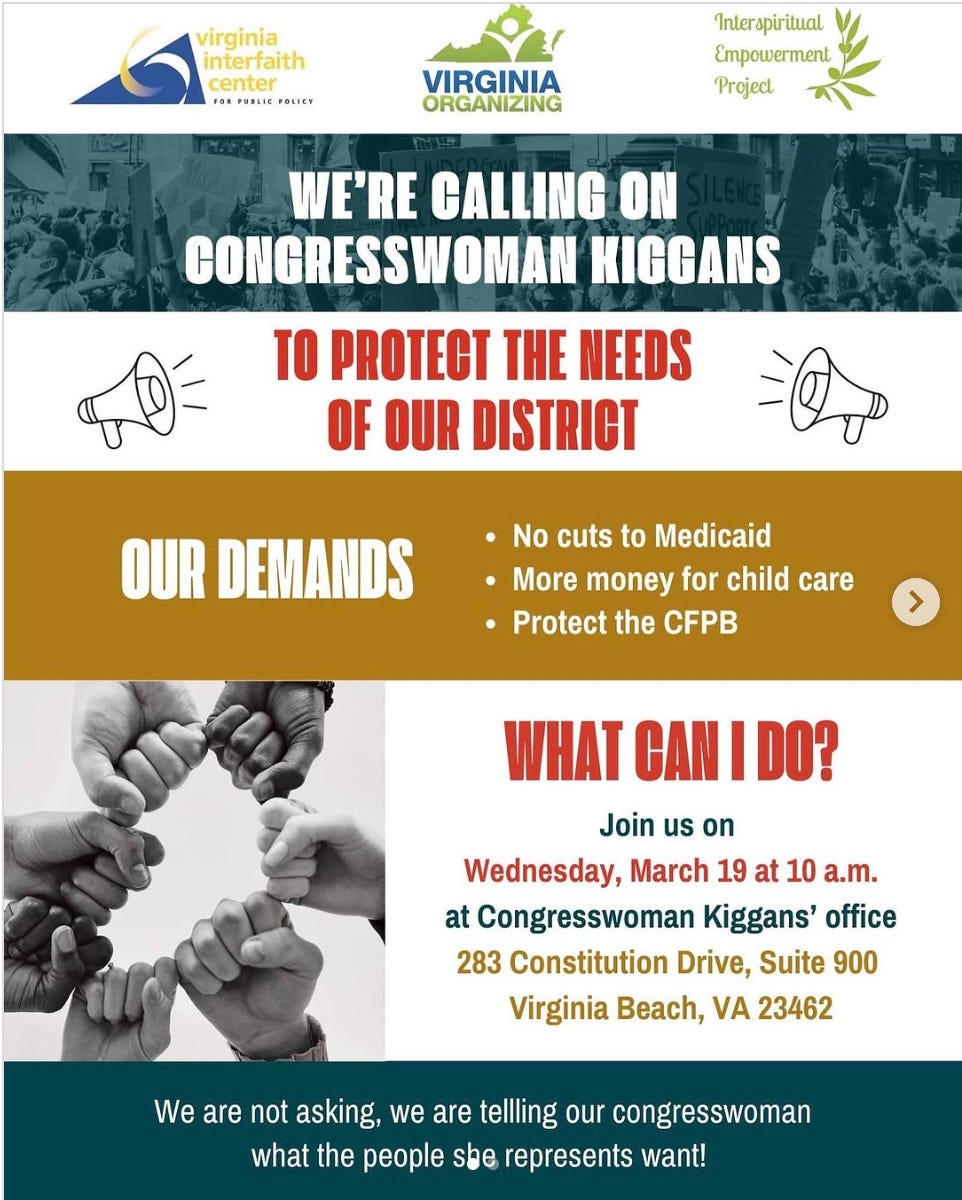

And Virginia Organizing hosted a gathering outside the office of Rep. Jen Kiggans to do the right thing by her constituents and defend the CFPB’s good work.

Important Notice from AFR: We are excited to announce that long-time economic justice advocate and AFR staffer Ericka Taylor has been named co-executive director of the organization, joining Lisa Donner in the role as Wall Street and various billionaires wield unprecedented levels of power. Congratulations to Ericka!

BANKING AND FINANCIAL STABILITY: Big Fraud – Michelle Bowman – Stop DOGE Overreach – What’s in a Crisis? – FTC Firings

CONSUMER: Bank Overdraft – Credit Union Overdraft – Medical Debt – Late Fees – Payday Lenders – Automakers and Big Tech Want to be Banks – FAIR in NY – Student Loans

CAPITAL MARKETS: UnFIRM Ground – The SEC Shake-up – The Billionaires’ Bill

PRIVATE MARKETS: Private Equity and Healthcare – Profit on Profit – PE Wants Your Golden Years – Walgreens

CRYPTO: GENIUS? Not Exactly – Trump and Binance – Crypto Politics – A Curious Crypto Cache – Crypto’s Revenge – Crypto in the House?

HOUSING: Agency Agitation – A Secret Mobile Home Enterprise – Mortgage Mayhem

CLIMATE AND FINANCE: An Imminent Danger – Profiting from Catastrophe – Trump’s Language Purge

Feedback? Reach us at afrnews@ourfinancialsecurity.org

BANKING AND FINANCIAL STABILITY

Big Fraud.

While Elon Musk’s DOGE and the wider Trump administration assault the agencies that would help defend people from scams – the CFPB and Securities and Exchange Commission (SEC), to name just two – the Federal Trade Commission reports that consumers lost $12.5 billion to fraud in 2024, including $5.7 billion stolen from investment scams alone.

Michelle Bowman.

Trump tapped Federal Reserve Governor Michelle Bowman to take Michael Barr’s position as vice chair for supervision, a role that would make her the central bank’s primary enforcer of Wall Street actors. The banking industry backs Bowman. Like many of them, Bowman opposed an early version of the Basel III Endgame bank capital rules, which would have improved the resilience of big banks.

Stop DOGE Overreach.

As DOGE and the broader Trump administration escalate their efforts to dismantle federal protections, labor unions and retirees are fighting back against DOGE’s unprecedented attempt to seize millions of Americans’ private Social Security data. A federal judge issued a temporary restraining order Thursday blocking DOGE from further access to any Social Security Administration systems that contain personally identifiable information.

What’s in a Crisis?

Looking back on the crisis that rattled the banking system in 2023, a working paper from the Chicago Fed points to the fact that the “crypto and VC sectors had a special role in triggering [the crisis] because the affected banks had business models focused on them.” Stepping beyond the unrealized losses and uninsured deposits on the now-collapsed banks’ balance sheets, the paper implicates cryptocurrency and venture capital for their instability and “empirically high level of volatility.” The researchers stress the need to analyze bank business models during supervision and note that having more liquid holdings can “be a stabilizing force…and can limit contagion.”

Meanwhile: Wall Street — both traditional banks and shadow banks — is a big fan of the same investment vehicles that tanked the economy in 2008: asset-backed securities and collateralized debt. S&P Global reports that structured credit bundles like these hit record levels in 2024 and may climb even higher this year.

FTC Firings.

This week, Trump illegally fired two Democratic Commissioners at the Federal Trade Commission, directly violating a Supreme Court precedent that prevents commissioners from being ousted over political disagreements. Said AFR’s Patrick Woodall:

This power grab, like so many others by Trump, subverts the rule of law and undermines the effectiveness of independent agencies that are designed to be more insulated from political and business pressures in order to protect the public interest. The commissioners Trump has illegally removed have a record of cracking down on rip offs in car sales, strengthening reviews of big corporate mergers to evaluate their impacts on consumers and workers, cracking down on Big Tech abuses, and protecting workers rights.

CONSUMER

Bank Overdraft.

Cadence Bank, a regional bank with hundreds of locations across the South, owes its customers $4.5 million as part of a class-action settlement for overcharging wrongful overdraft fees. Between January 2019 and November 2023, some account-holders were charged an unrefunded “Authorize Positive, Settle Negative” fee – an overdraft fee – on debit transactions they initiated with a positive balance that later settled negative. The bank also agreed to forgive up to $682,000 in unpaid fees.

Credit Union Overdraft.

National Credit Union Administration board members Tanya Otsuka and Todd Harper criticized a recent decision by Chairman Hauptman not to publish overdraft and non-sufficient fund fee income for individual member unions. Otsuka calls it a “step in the wrong direction,” warning of a lack of transparency that would let larger financial institutions “that rely heavily on fee income to operate in the shadows, resulting in less competition and less choice for consumers.” Indeed, some credit unions have raked in millions in profit from predatory overdraft.

Medical Debt.

Congressional Republicans have advanced measures (H.J.Res.74 and S.J.Res.36) to roll back the CFPB’s medical debt rule, which would have erased more than $49 billion in medical debt from the credit reports of 15 million people. AFR’s Amanda Jackson writes:

The people who rack up medical debt are sicker, have jobs with worse health insurance coverage, and have lower incomes and household wealth. Medical debt essentially reinforces and amplifies the racial inequalities in the economy and the financial system…The Republican effort to overturn the medical debt rule effectively punishes people for having medical needs and emergencies. The patchwork health insurance system, without comprehensive public healthcare coverage, means that the negative impact of medical debt on families’ falls hardest on those who need access to the financial system the most—while the credit reporting industry profits.

Late Fees.

Acting CFPB Director Russell Vought wants to find a way out of defending the CFPB’s rule capping credit card late fees at $8 in a Texas federal court. Bowing to industry, the agency’s legal counsel says it “respects this Court’s ruling granting a preliminary injunction” and believes the industry associations’ claims have “merit.” Said AFR’s Christine Chen Zinner:

The big Wall Street banks had been leading the charge against lower credit card late fees and now Trump appointees have joined them in trying to destroy this valuable consumer protection…Trump-appointed judges were already at work trying to make life more expensive for everyone who has a credit card. Now the Trump administration owns this move as well.

Payday Lenders.

After the Supreme Court last year denied the payday lobby’s argument against a portion of the CFPB’s payday rule – which prevents high-cost lenders from continuing to try taking money from customers’ accounts after transactions have been declined a certain number of times. The rule was slated to take effect on March 30, 2025. This month, the Community Financial Services Association filed a petition for certiorari to continue their fight at SCOTUS.

Automakers and Big Tech Want to be Banks.

Eager to take advantage of lighter-touch regulations, the Big Three automakers are trying to get the greenlight to control so-called industrial banks. These institutions would allow the likes of General Motors (GM), Ford and Stellantis to accept deposits and offer financial services to their customers, potentially exposing consumers and the system to greater instability and risk. During the 2008 financial crisis, a bank previously owned by GM toppled and necessitated a taxpayer-funded bailout.

Said George Washington University’s Arthur Wilmarth:

This has the clear potential to transform the nature of our banking system in ways that would be very harmful to consumers and very threatening to our economy. If federal regulators approve the automakers’ applications, how could they turn down similar requests from a Big Tech firm like Apple, Google, Amazon or Facebook?

Speaking of Big Tech: The Electronic Privacy Information Center and AFR oppose efforts by Congress to overturn finalized CFPB rules that would protect users of payment apps.

FAIR in NY.

As the Trump administration weakens federal consumer protections, New York Attorney General Letitia James and state lawmakers unveiled a new bill aimed at protecting consumers and small businesses from deceptive, unfair, and abusive practices. The legislation strengthens outdated consumer protection laws to combat scams like deed theft, hidden junk fees, predatory lending, and hard-to-cancel subscriptions. It also empowers the Attorney General’s office to hold bad actors accountable and seek restitution for victims.

Student Loans.

The American Federation of Teachers (AFT) is suing the U.S. Department of Education for unlawfully blocking access to income-driven repayment (IDR) plans and Public Service Loan Forgiveness (PSLF), jeopardizing millions of borrowers' ability to afford student loan payments and unfairly punishing millions of borrowers left in financial limbo. Three weeks ago, the Trump administration abruptly removed IDR applications from the Department’s website and ordered servicers to halt processing, effectively freezing the student loan system. IDR plans are a critical tool for tying loan payments to income and are essential for public service workers seeking PSLF relief. The lawsuit, filed in federal court, demands the restoration of borrowers' legal rights to affordable repayment options.

CAPITAL MARKETS

UnFIRM Ground.

The Senate Banking Committee should not help the big industry actors crying wolf, according to a letter from AFR and partners about the FIRM Act. While the bill purports to curb banking discrimination, it would do nothing to prevent actual discrimination or improve access to financial services for people in protected classes. What it would do, however, is upend the longstanding framework of bank supervision and regulation. The Senate Banking Committee voted to advance the bill on a party-line vote. To learn more about what’s behind industry cries of alleged “debanking,” watch a webinar on the topic featuring Graham Steele, former Assistant Secretary of Financial Institutions at Treasury.

The SEC Shake-up.

A group of Democrats from the House Financial Services Committee wants answers from SEC Acting Chair Uyeda about why the agency plans to close three of its regional offices by the end of the summer. They write: “This regional presence ensures timely intervention and allows the SEC to address a wide variety of issues across the country, from helping local small-businesses access needed capital to examining SEC registrants, to bringing enforcement actions against bad actors.”

The Billionaires’ Bill.

AFR, the Consumer Federation of America, and Public Citizen led a letter to Delaware lawmakers opposing Senate Bill 21. Referred to by some as the Billionaires’ Bill, this legislation would undermine the ability of regular shareholders, like teachers and firefighters saving for retirement, to hold directors, officers, and controlling stockholders like Elon Musk and Mark Zuckerberg accountable through the Delaware Courts when they overreach and extract value from companies incorporated in Delaware. The signatories note that the legislation would undermine retirement security and corporate accountability, and according to many institutional investors, turn Delaware into a “less attractive state for incorporation.”

According to a poll released by Americans for Financial Reform and American Association for Justice, only 16 percent of voters want the Billionaires’ Bill to pass as is and 63 percent are less likely to vote for legislators who back it as is.

PRIVATE MARKETS

Private Equity and Healthcare.

AFREF provided testimony in support of a Connecticut bill that would improve oversight of private equity healthcare acquisitions:

The financialization of healthcare worsens access to care, raises prices for treatment and care for patients, worsens the rights of medical professionals and other workers in private equity-owned healthcare facilities, and due to their asset-stripping practices, can reduce the access to care when private equity-owned facilities are led into bankruptcy.

Axios offers a roundup of states that have advanced legislation to curb private equity’s buyout of the healthcare sector. At least 13 states have introduced related bills recently, as scrutiny mounts after high-profile bankruptcies (like Steward Health) and evidence accrues of higher medical debt and lower care quality among private equity-backed facilities.

Profit on Profit.

At a summit held by the American Federation of Teachers, AFR’s Oscar Valdés Viera raised concern about the carried interest loophole. The fees they reap from their investment services are taxed as capital gains – not as income. As a result, the clients, including the pension funds that manage the retirement savings of those same working families, can be left holding the bag after private equity’s moral hazard and excess risk-taking. Said Valdés Viera:

It is important to note that while pension funds pay carried interest fees to private equity firms, they receive no benefit from the loophole itself. In short, closing the carried interest loophole is a crucial step to unrigging a tax code that rewards wealth over work, fuels inequality, deprives governments of critical revenue, and distorts economic incentives. Ending this loophole would better protect workers from the fallout of private equity’s risky investment practices.

PE Wants Your Golden Years.

Private equity’s growing push into workplace retirement plans poses significant risks for everyday investors, as these high-fee, high-risk, opaque investments could jeopardize workers’ hard-earned savings. Despite making up less than 1 percent of defined contribution assets, firms like Apollo, Blackstone, and KKR are aggressively seeking access to the $12.5 trillion retirement market. Critics warn about private equity's lack of transparency, illiquidity, high fees, and legal risks associated with their volatile, high-cost investments.

Walgreens.

Walgreens' recent $10 billion buyout by private equity firm Sycamore Partners highlights the financial challenges plaguing the pharmacy industry. The acquisition comes as the pharmacy sector faces mounting difficulties, including high employee turnover, declining reimbursement rates, and shifting consumer preferences toward mail-order services. Like CVS and Rite Aid, Walgreens has struggled to maintain profitability amid these pressures, with retail sales suffering due to competition from e-commerce giants like Amazon. AFR’s Aliya Sabharwal noted: “Sycamore’s retail takeovers have not turned out well for retail chains, workers, or shoppers. The private equity playbook is good for lining Wall Street executives’ pockets but is bad for workers and the industries they pillage.”

CRYPTO

GENIUS? Not Exactly.

Last week, Republicans (and a handful of Democrats) on the Senate Banking Committee advanced the GENIUS Act, a bill that tries to legitimize risky stablecoins and embed them more deeply into the banking system, at great risk to investors and the economy at large. Said AFR’s Mark Hays:

By voting for this bill, Members of Congress are in danger of ignoring the regulatory mistakes of the past by adopting light touch regulations that could amplify systemic risk and increase the chances that the next crypto crash will reverberate across the financial system, harming crypto investors and the real economy…Senators should stand up to the crypto broligarchy and its gusher of campaign cash because if this bill passes, the next crypto catastrophe could trigger a financial meltdown that will rival or eclipse the 2008 financial crisis.

Trump and Binance.

World Liberty Financial, a crypto venture steered by the Trump family, has been in talks with the cryptocurrency exchange Binance, whose founder was sentenced to prison last year after pleading guilty for failing to prevent money laundering. According to insiders, the discussions have included the possibility of Binance creating a stablecoin with World Liberty, as well as the potential for World Liberty to claim a stake in Binance's U.S. arm.

Speaking of Binance: A $2 billion investment from an Abu Dhabi-based MGX earlier this month marked the very first institutional investment in Binance, and it was made in an unnamed stablecoin.

Crypto Politics.

The Center for Political Accountability's report, Risky Return: The True Price of Crypto’s Political Spending Spree, outlines the cryptocurrency industry’s aggressive political influence campaign. Crypto firms poured over $134 million into the 2024 election cycle, yet this strategy comes with significant downsides, including heightened regulatory scrutiny, reputational damage, and legal vulnerabilities.

A Curious Crypto Cache.

Earlier this month, Trump signed an executive order to create a strategic cryptocurrency reserve, propping open the door for potential conflicts of interest. Days later, Sen. Lummis unveiled a bill that proffers a more expansive version of Trump’s idea. Crypto researcher Molly White suggests that it largely “appears to be a government policy crafted solely to benefit a small group of wealthy speculators and crypto companies.”

Crypto’s Revenge.

In Trump’s pro-crypto political moment, cryptocurrency executives are eager to take revenge on the SEC, the agency that during the last administration put guardrails on the industry’s risky practices. Politico lowlights Coinbase CEO Brian Armstrong and Ripple lawyer Stuart Alderoty’s suggestion for industry not to hire SEC lawyers who were involved in enforcement, and the Winklevoss twins’ call for the agency to fire and shame the employees who worked on the case against their company Gemini.

Crypto in the House?

The U.S. Department of Housing and Urban Development (HUD) is considering incorporating cryptocurrency technology into its operations, sparking significant internal concerns. While officials claim the initiative is primarily about using blockchain to track federal grants, skeptics fear it could be a Trojan horse for broader crypto adoption in government—despite the technology’s association with financial speculation, regulatory uncertainty, cybersecurity risks from hacks and scams, and even criminal activity.

HOUSING

Agency Agitation.

Last week, Trump appointee Bill Pulte was sworn in to serve as the director of the Federal Housing Finance Agency, the government entity responsible for ensuring liquidity and stability in the mortgage industry. One of his first moves: an unprecedented power-grab; Pulte ousted 14 members from the boards of Freddie Mac and Fannie Mae and named himself chairman of both companies. Already, the FHFA has cut 10 percent of its jobs and has demanded that the remaining employees end teleworking.

At the Department of Housing and Urban Development (HUD), Congressional Democrats reminded Trump-appointed Secretary Scott Turner that, despite action taken by the administration to undermine enforcement of housing civil rights laws, his agency still has a mandate to “enforce the law, including by investigating housing discrimination complaints which are at an all-time high.”

A Secret Mobile Home Enterprise.

Enterprise Community Partners is a nonprofit lender ostensibly focused on increasing affordable housing supply, building upward mobility, and centering racial equity. But Shelterforce calls into question ECP’s majority ownership of Bellwether Enterprise, a lender that finances massive acquisitions of manufactured home communities, i.e. mobile home parks. One of these creditees, Havenpark, is a private equity investment firm notorious for rent hikes and muscling out buyers who wanted to convert their neighborhood into a cooperative.

Said AFREF’s Caroline Nagy:

If you are participating in an affordable housing preservation program and the outcome of your program is seeing very high housing cost increases and evictions and displacement, you are not running an affordable housing preservation program—you’re doing something else…We have to first acknowledge that it is not in the legitimate public interest to provide lower cost financing to private equity firms so that they can displace people, raise costs, and make more money for themselves. The problems with manufactured housing have been so flagrant—abuses, frankly, of the folks who live in these communities. It is shocking that a federal government program would do this to people.

Mortgage Mayhem.

As the Trump administration works to gut the CFPB, the industry is concerned about how it will affect the mortgage market – from dismissal of seasoned staff that have long worked on mortgage issues to the cancellation of contracts with firms that collect mortgage data.

CLIMATE and FINANCE

An Imminent Danger.

This week, AFR published a policy memo on the climate crisis. The memo emphasizes that climate change is not just an environmental issue but a looming economic and financial crisis that is already wreaking havoc. The rising costs of climate disasters are staggering: in 2024 alone, the U.S. faced 27 extreme weather events, each causing over $1 billion in damages. Meanwhile, recovery costs continue to outpace insurance coverage, leaving individuals, businesses, and governments increasingly exposed. Climate-related risks are driving up home insurance premiums, inflating mortgage delinquency rates, and threatening to erode $1.47 trillion in U.S. home values by 2055.

Financial institutions are also deeply vulnerable to both the physical impacts of climate change—like wildfires and floods—and the transition risks of a rapidly changing energy economy. Yet instead of addressing these threats, the incoming Trump administration is dismantling critical climate safeguards and undermining the independence of financial regulators. To protect the economy and peoples’ financial futures, policymakers and advocates must resist these rollbacks, defend regulatory independence, and ensure financial institutions are prepared to manage climate-related financial risks.

Profiting from Catastrophe.

Catastrophe bonds are a type of security issued by insurance companies that want to share the risk of major disasters with investors who are willing to shoulder the high burden in exchange for high return. When a predefined event happens, like a hurricane or earthquake of a certain size, the bond pays out to the insurer. Next month, the very first exchange-traded fund (ETF) for catastrophe bonds will be launched, exposing more investors to the growing risk of climate-intensified natural disasters.

Trump’s Language Purge.

According to Grist, the Trump administration is making it harder to discuss and address pressing climate issues by directly censoring certain words: federal websites are shedding mentions to the phrases “clean energy,” “sustainability,” and even “resilience.”